The Crossroads Of Estate Planning & Immigration:

Key Concepts In International Estate Planning

International estate planning is a growing trend for many families in the United States and throughout the world. Unfortunately, some families don’t realize the legal issues involved in their estate plan until it is too late to take advantage of the planning opportunities. Without some familiarity with the legal issues, it may not be immediately obvious when an international approach to estate planning is needed. Fortunately, this is something that we have given a lot of time to understanding. We have posted about this information in the past. This article introduces a few key concepts that every international family should understand and includes some updated information for 2023:

1. Permanent Resident Status, Tax Residency, Domicile, & Citizenship: How Do These Concepts Affect My Estate Plan?

In every-day conversation, the terms “domicile” and “residence” are used interchangeably to refer to the place someone lives, but as legal concepts, these terms very specific meanings. Adding further confusion, U.S. immigration law and the tax code each have separate standards for determining residency.

For example, under U.S. immigration law, the standard for residency is whether someone is a Lawful Permanent Resident (LPR). LPRs (also referred to as “green card holders”) have gone through the immigration process to become permanent residents. This status allows living and working permanently in the United States.

For tax purposes, the U.S. tax code treats any non-U.S. citizen as either a “Resident Alien” and Non-resident Alien.” Under this framework, the category of Resident Alien includes anyone who has a green card (an LPR as described above), but also anyone who meets a “substantial presence test.” This means that even those who are not green card holders, who are not allowed to live permanently in the United States and who may not even have authorization to work in the United States, can still be taxed as residents if they spend significant time in the United States.

Finally, the tax code treats domicile separately as well. One’s domicile is, “an individual’s fixed or permanent home” which is acquired by “living there; even for a brief period of time, with no definite present intention of later removing therefrom.”

Accordingly, it is possible to be domiciled in the United States without being a resident. And it is possible to be taxed as a resident even without a green card.

This article will discuss some of the ways these concepts can impact your overall estate plan. However, it is important to note that these differences in terms can sometimes lead to confusion and missteps for anyone who is not careful.

2. Tax Rules For International Families

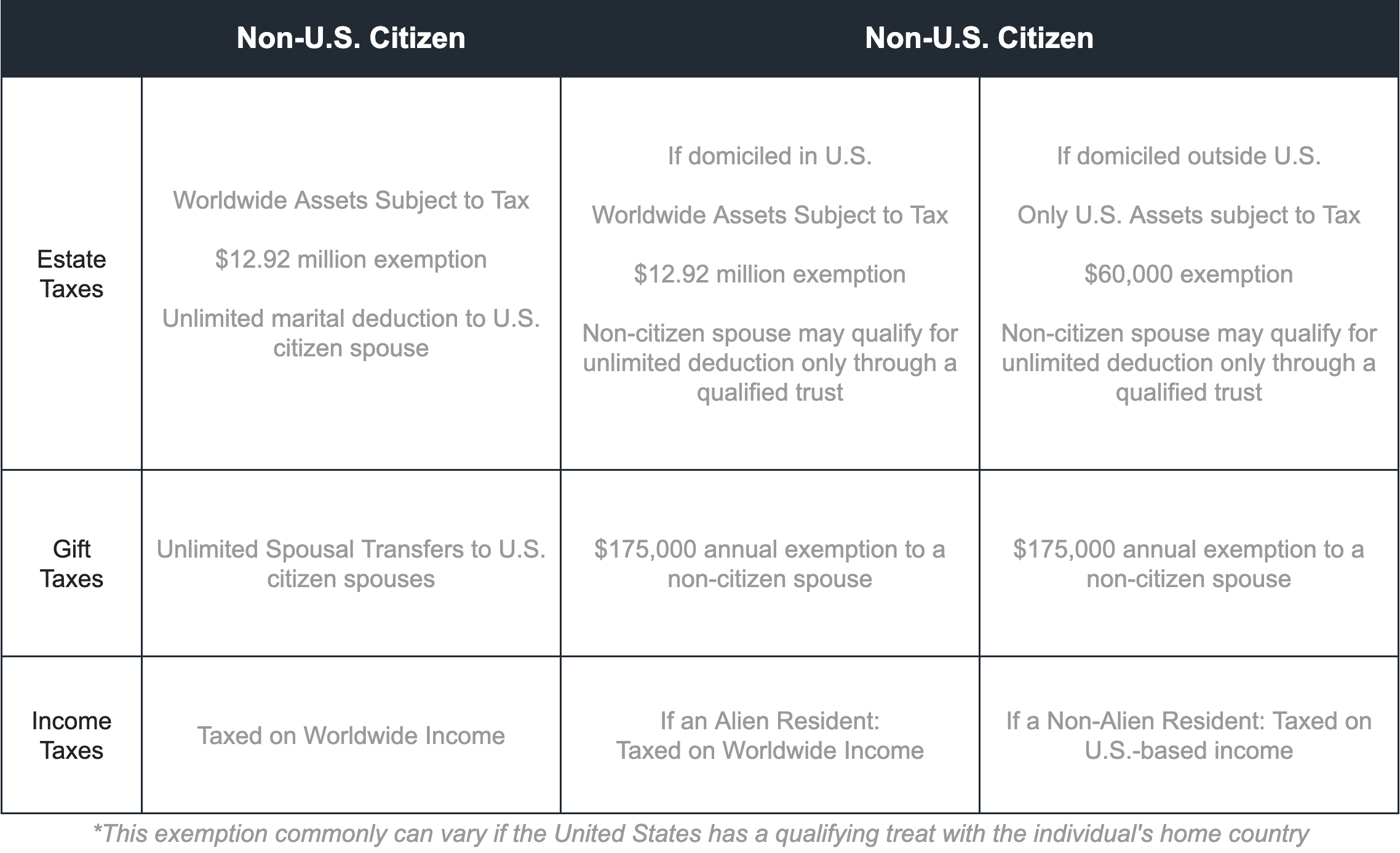

Historically, tax planning has always been an important part of estate planning. This continues to b the case as estate and gift tax rates currently reach as high as 40%. There are a number of potential exemptions from these taxes, but eligibility for these exemptions can vary—especially for international families. For example, U.S. citizens and those who are domiciled in the United States are currently allowed an estate tax exemption of $11.7 million, but that exemption amount drops to only $60,000 for those not domiciled in the United States. Additionally, U.S. spouses can make unlimited gifts to each other during their lifetimes and at death, but this unlimited marital deduction is not available if the receiving spouse is not a U.S. citizen. Instead, non-citizen spouses are entitled to annual exemption of up to $155,000 per year. These key tax rules are outlined in the table below:

A well-designed estate plan for an international family will take these rules into consideration in determining how to distribute family assets. For example, a non-citizen spouse can inherit assets through a Qualified Domestic Trust (QDOT) free of estate or gift taxes. Additionally, families may decide to include long-term gifting as a part of the estate plan to take advantage of annual gift tax exclusions as a way to avoid future estate taxes.

3. Pre-Immigration vs. Post-Immigration Options

An often-overlooked part of estate planning for international families includes a careful analysis of tax options before immigrating to the United States. As described above, those who are not yet residents of the United States and not are not yet domiciled in the United States are not subject to U.S. taxes (unless their assets or sources of income originate in the United States). This allows for tax planning strategies that may not be available once a family establishes roots in the United Sates. Working with a qualified tax advisor, international families may opt to sell certain assets or make gifts prior to arriving in the United States.

Additionally, for international families that have already established a close connection to the United States, estate planning and immigration decisions should be made carefully (with the advice of qualified professionals). Specific provisions may vary widely depending on a family’s long-term goals. For example, the decision whether to seek permanent resident status or naturalization in the United States may have tax and estate planning implications: a non-U.S. citizen who intends to receive a large inheritance from a spouse may decide to pursue naturalization to become a U.S. citizen as soon as possible. On the other hand, for family members who do not intend to live permanently in the United States, a plan may not include long-term trusts in the United States that will unnecessarily subject your beneficiaries to U.S. tax laws.

In any case, a qualified international estate planning attorney can help you identify important issues and can design plan that meets your family’s needs.

4. Coordinating Across Jurisdictions

Tax and inheritance laws can vary substantially from one country to another. When planning for family members (or property) in our multiple countries, it is important to make sure that your overall estate plan is coordinated across each jurisdiction.

For example, as noted above, the U.S. tax regime includes various exemptions from estate taxes. When estate taxes are applicable, they are paid by the estate level—usually by a Trustee or Personal Representative of the estate before assets are distributed to individual beneficiaries. In some other countries, however, inheritance taxes are paid by the person who receives the inheritance. This difference in approach can create significant problems if the estate is administered in one jurisdiction and the beneficiary is living in another.

Succession laws can vary around the world as well. In the United States, most jurisdictions have “rules of intestacy” which dictate who inherits when there is no plan, but families are free to plan around those rules when designing their estate plan. (While some states have specific protections in place for a spouse or minor child, most U.S. estate plans are free to include or disinherit whomever they choose). This is not the case in all countries around the world. Many jurisdictions have “forced heirship” laws that dictate which family members can or cannot inherit.

For complex issues such as these, it is important to work with a team of advisors who are experienced in spotting potential issues and who are wiling to coordinate with other advisors as necessary. It is rare to find an individual attorney (or law firm) with deep expertise in multiple jurisdictions. However, experienced international advisors are generally committed to working along with a team of other professionals to coordinate high-quality planning strategies for international families.

5. The Need To Regularly Update An International Estate Plan

Whenever there are changes in the law and family circumstances, it is important to update your estate plan. When your family situation includes international concepts like dual citizenship, residency, or domicile; or if you own assets in multiple jurisdictions, it becomes even more important to ensure your plan is kept up to date. Laws change. Family members move and change status. Your estate plan should keep up with those changes.

At the Gunderson Law Group, P.C., we strongly recommend that you meet with your estate planning attorney and other advisors on a regular basis (at least annually) to ensure your plan is kept up to date. We are excited to be rolling out new tools to help our clients stay up to date and “in the know” as changes develop. As always, we invite you to reach out to us directly if you have specific questions.

Approved and published by Adam Gunderson

Arizona Location

1400 E. Southern Ave. Suite 850

Tempe, AZ 85282

Office: (480) 750-7337

Email: [email protected]

{kind=link}

{kind=link}